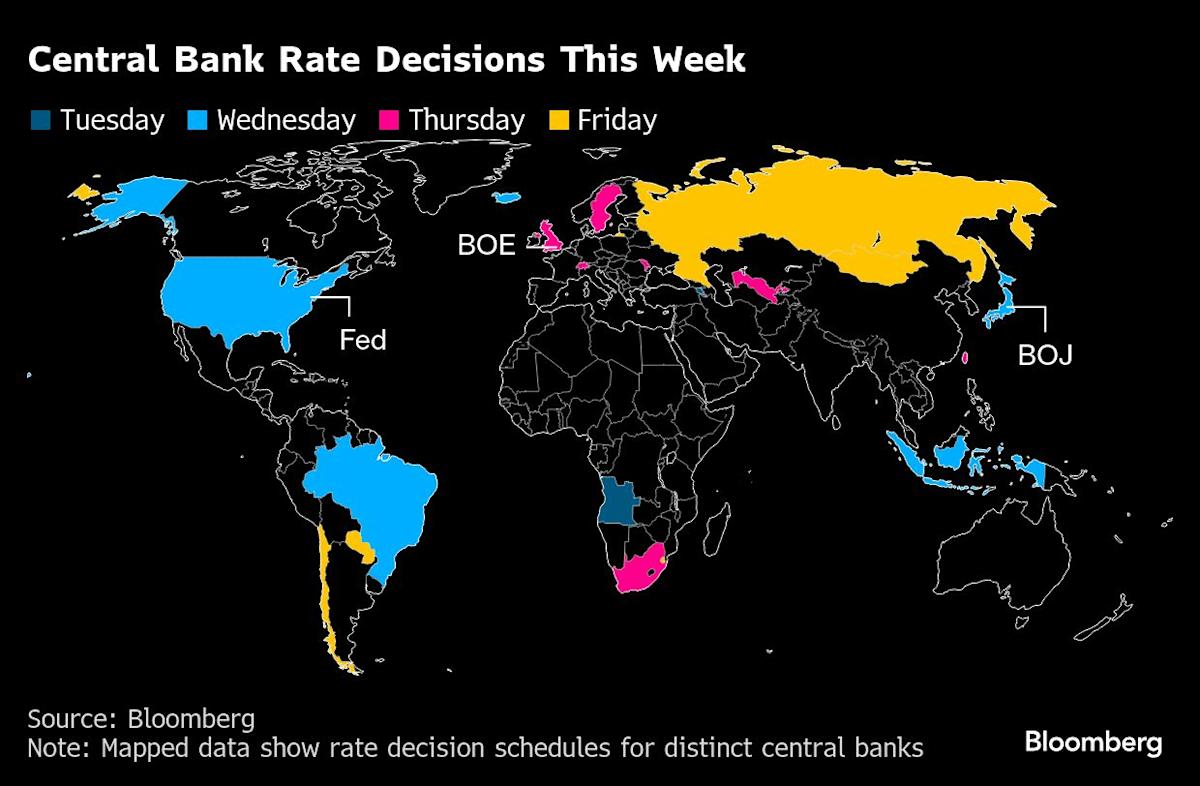

(Bloomberg) — An anxious sense of wait-and-see may emerge from central banks in the coming week, in their first collective assessment of how President Donald Trump’s trade policies are impacting the world economy.

Most Read from Bloomberg

While officials from Washington to London and Tokyo have already set borrowing costs once since the US president entered the White House in January, those decisions preceded a marked escalation in his rhetoric and measures against neighbors, allies and competitors alike.

With global tariffs now in place on steel and aluminum, and with Canada, China and the European Union all further suffering Trump’s ire, what were unrealized threats a few weeks ago have now emerged as full-blown hindrances to commerce.

Central bankers struggling to gauge whether the impact will be greater on growth or inflation may well choose to do nothing for now.

New-found worries about a potential US recession that gripped Wall Street in the past week probably won’t spur the Federal Reserve to deliver more easing for now, and unchanged interest rates are also the most likely outcomes at meetings in Japan, the UK and Sweden. Officials in South Africa, Russia and Indonesia may follow suit.

Some others will probably act immediately, though, against pressing risks — while warily assessing the shockwaves of Trump’s actions. In Brazil, for example, the central bank is widely anticipated to raise borrowing costs again to fight resurgent inflation.

What Bloomberg Economics Says:

“Even as consumer and business confidence deteriorate quickly, the Fed’s degree of freedom to cut rates is constrained by indicators showing a surge in inflation expectations. In the absence of a ‘Trump Put,’ the Fed’s reluctance to cut – to offer the market a ‘Fed Put’ at least – could push the downturn in sentiment into something beyond just vibes.”

—Anna Wong and Chris G. Collins, economists. For full analysis, click here

In all, officials responsible for half of the world’s 10 most-traded currencies, along with other Group of 20 peers, are poised to set rates over the coming days.

European Central Bank President Christine Lagarde on Wednesday described the challenge confronted by many of global counterparts. With her own institution recently having stopped short of signaling its next move out of caution about the backdrop, she says the job of monetary policymaking just got harder.

“The level of uncertainty we are facing is exceptionally high,” Lagarde said. “Maintaining stability in a new era will be a formidable task.”

Click here for what happened in the past week, and below is a closer look at the panoply of central-bank decisions due in the coming days.

US

With Fed officials expected to hold rates steady on Wednesday at the conclusion of their two-day meeting, the market will focus on officials’ updated economic projections and Chair Jerome Powell’s press conference for clues about the path ahead.

Economists expect officials to lower borrowing costs twice this year, starting in September, according to a Bloomberg survey. For now, policymakers have signaled they’re in a wait-and-see mode as they seek further progress on inflation and greater clarity on the economic impact of Trump’s policies.

Powell emphasized this month that the Fed doesn’t need to be in a hurry to cut rates. But amid a recent selloff in stocks paired with mounting growth concerns and souring consumer sentiment, the Fed chief will likely be pressed on whether the central bank will be ready to step in should the economy turn south.

Asia

Japan

The Bank of Japan is widely expected to hold rates steady on Wednesday as authorities assess the impact of their January hike, with the focus falling on whether persistent yen weakness, high inflation and robust wage gains may open the door to a hike on May 1.

About half of surveyed economists say such an increase won’t come until July, though.

Indonesia

Indonesia’s central bank on Wednesday may continue to pause its easing cycle. Monetary authorities are aiming to limit capital outflows after the rupiah faced renewed pressure following the decision to keep rates on hold in February.

China

A day later, lenders in China, with guidance from the central bank, are expected to hold the 1-year and 5-year loan prime rates steady. That will follow data earlier in the week likely to have been distorted by the Lunar New Year holiday, with economists anticipating a 5% year-on-year increase in industrial production, a moderated decline in property investment, and increases in both retail sales and fixed asset investment.

Taiwan

Taiwan’s central bank decision is also due on Thursday, and officials in Taipei are expected to keep the benchmark rate at 2% for a fourth straight meeting.

Europe, Middle East, Africa

UK

The Bank of England is set to hold fire on another cut on Thursday. That would leave its rate at 4.5% as it sticks to a gradual, once-a-quarter pace for reductions.

While the latest growth data showed a surprise contraction, the BOE’s Monetary Policy Committee is likely to prime investors for a cautious approach to further easing in the face of mounting geopolitical tensions, stubborn price pressures, and uncertainty over the impact of the Labour government’s first budget.

Dissenting policymakers may back an immediate rate cut, but other officials on the panel with a dovish leaning have signaled increasing hesitancy in recent weeks.

Switzerland

In contrast with its advanced-economy peers, the Swiss National Bank’s decision on Thursday is laden with suspense.

Many forecasters anticipate a final quarter-point reduction, to 0.25%, to cushion growth from a global backdrop of likely Trump-induced economic weakness.

But with less pressure on the franc for now, the need to preserve precious ammunition for future easing as a shield against currency inflows could persuade officials to keep borrowing costs unchanged.

Sweden

The Riksbank is set to hold its rate at 2.25% after five consecutive cuts. Officials have signaled a preference to gauge the lagged impact of those steps on a tepid economy, and faster-than-expected inflation may have further cemented that view.

Other data have been contradictory. Sweden’s gross domestic product rose the most in 2 1/2 years during the fourth quarter, but survey indicators point to weakness.

Analysts have increasingly dropped predictions for one more quarter-point move this easing cycle, while overnight swaps now price in only three basis points of cuts by the August meeting, down from 38 basis points seen at the end of last month.

South Africa

After three successive hikes, South African policymakers may keep their rate at 7.5% on Thursday as they weigh the impact of global tariffs on their inflation forecasts. Neighboring Eswatini, whose currency is pegged to the rand, may also hold the following day.

Russia

With inflation having risen above 10% in February, the Bank of Russia will assess the need on Friday for another hike in its rate, which has been at a record high 21% since October. Bloomberg Economics expects policymakers to opt for a third consecutive hold.

Angola

The central bank will likely leave its key rate unchanged at 19.5% for a fifth meeting in a row on Tuesday as officials try to curb high inflation.

Morocco

Policymakers cut the base rate by 25 basis points to 2.5% in December. Since then, inflation has accelerated from under 1% to about 2%, which may cause them to hold off easing again on Tuesday.

Iceland

The central bank in Reykjavik may slow the rate of easing at its second decision of the year on Wednesday. Local lenders Landsbankinn hf and Islandbanki hf both predict a quarter-point reduction, to 7.75%.

Latin America

Brazil

Banco Central do Brasil’s March meeting on Wednesday will be missing some of its usual drama, as policymakers have telegraphed they’ve lined up a third straight 100 basis-point rate hike, to 14.25%. Analysts and traders expect it to end 2025 at 15%.

Chile

Sticky and stubbornly elevated inflation, risks skewed to the upside, and wobbles in expectations persuaded Chile’s central bank to keep its 5% rate unchanged in January.

A slight slowdown in February consumer prices data, putting the annual rate at 4.8%, likely headed off a hike for this Friday, but strong domestic demand argues against any easing. In fact, traders are expecting no change in policy for the next 12 months, while local analysts see room for 50 basis points in cuts.

Argentina

Since President Javier Milei took office in December 2023, the Argentine central bank’s rate moves have often come in close proximity to monthly inflation reports.

After February data’s released on Friday, Argentina watchers are on alert for the bank’s 10th rate cut under Milei. It’s one of the more unorthodox elements of the president’s strategy to slow inflation in South America’s No. 2 economy.

Paraguay

Paraguay’s central bank has kept borrowing costs unchanged at 6% since delivering a quarter-point cut a year ago, but February’s jump in headline inflation to 4.3% may bolster the hawkish case at this week’s policy meeting.

–With assistance from Brian Fowler, Monique Vanek, Ott Ummelas, Paul Wallace, Ragnhildur Sigurdardottir, Reade Pickert, Robert Jameson, Tom Rees, Tony Halpin and Vince Golle.

Most Read from Bloomberg Businessweek

©2025 Bloomberg L.P.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  XRP

XRP  BNB

BNB  Solana

Solana  USDC

USDC  Dogecoin

Dogecoin  Cardano

Cardano  Wrapped Bitcoin

Wrapped Bitcoin  Sui

Sui  Wrapped stETH

Wrapped stETH  Avalanche

Avalanche  Hyperliquid

Hyperliquid  Stellar

Stellar  Shiba Inu

Shiba Inu  LEO Token

LEO Token  Hedera

Hedera  Bitcoin Cash

Bitcoin Cash  Toncoin

Toncoin  Litecoin

Litecoin  Polkadot

Polkadot  USDS

USDS  WETH

WETH  Binance Bridged USDT (BNB Smart Chain)

Binance Bridged USDT (BNB Smart Chain)  Wrapped eETH

Wrapped eETH  Pepe

Pepe  Pi Network

Pi Network  Ethena USDe

Ethena USDe  Coinbase Wrapped BTC

Coinbase Wrapped BTC  WhiteBIT Coin

WhiteBIT Coin  Bittensor

Bittensor  Aave

Aave  NEAR Protocol

NEAR Protocol  Aptos

Aptos  OKB

OKB  Jito Staked SOL

Jito Staked SOL  Ondo

Ondo  BlackRock USD Institutional Digital Liquidity Fund

BlackRock USD Institutional Digital Liquidity Fund  Gate

Gate  Official Trump

Official Trump  VeChain

VeChain  Ethena Staked USDe

Ethena Staked USDe  sUSDS

sUSDS  Render

Render  Ethena

Ethena  USD1

USD1  Cosmos Hub

Cosmos Hub  POL (ex-MATIC)

POL (ex-MATIC)  Artificial Superintelligence Alliance

Artificial Superintelligence Alliance  Fasttoken

Fasttoken  Algorand

Algorand  Filecoin

Filecoin  Arbitrum

Arbitrum  Celestia

Celestia  Worldcoin

Worldcoin  Jupiter Perpetuals Liquidity Provider Token

Jupiter Perpetuals Liquidity Provider Token  Binance-Peg WETH

Binance-Peg WETH  KuCoin

KuCoin  Maker

Maker  Bonk

Bonk  Jupiter

Jupiter  Binance Staked SOL

Binance Staked SOL  Quant

Quant  Story

Story  Flare

Flare  NEXO

NEXO  Fartcoin

Fartcoin  Immutable

Immutable  Rocket Pool ETH

Rocket Pool ETH  Optimism

Optimism  Injective

Injective  Virtuals Protocol

Virtuals Protocol  USDT0

USDT0  Solv Protocol BTC

Solv Protocol BTC  The Graph

The Graph  dogwifhat

dogwifhat  Mantle Staked Ether

Mantle Staked Ether  Curve DAO

Curve DAO